The post Amazon Physical Stores: A Successful Game Changer in the Retail Sector? appeared first on Apocalypse Retail.

]]>We want to give our special thanks to Pablo Marcote & Ricard Codina, the two students who co-authored this post.

Sometimes, big isn’t big enough. For Amazon, the world’s most significant e-commerce player, the online world isn’t enough to contain its ambitions.

Amazon physical stores are part of the company’s well-planned entry into the retail landscape. And like everything it has touched, Amazon has all the expertise and financial punch to change the brick and mortar sector.

Shopping and Amazon are synonymous. But for a while now, it’s the company that’s been on a shopping spree.

This shopping spree is different from Jeff Bezos’s post-divorce purchases of a yacht that comes with another yacht or a mansion with a 9-hole golf course. No, this is about the company and not the new bachelor on the scene.

From Whole Foods to PillPack to Ring to Zoox, the online behemoth has acquired companies to build its portfolio, enhance its technological capabilities, and fuel its retail growth. As a result, its strategy is different from other online or big-box retailers.

What is Amazon’s physical store strategy?

The company has been rolling out Amazon physical stores to widen the horizon of its offerings in the retail sector.

Amazon Go, Amazon Go Grocery, Amazon 4-Star, and Amazon Lockers are only some moves to disrupt the market and enhance offline shopping experiences.

After redefining e-commerce, the company, it seems, is now about to redefine commerce as we know it.

Amazon Books, the company’s first venture into the traditional retail sector, was launched in 2015.

Starting in Seattle, it’s now present all across America. The Whole Foods acquisition followed suit. Then came Amazon Go, Amazon Go Grocery, and others. With Whole Foods, the company now has around 600 physical stores worldwide, divided as follows:

The strategy is to be an omnichannel marketplace instead of a single-channel seller.

After a testing phase opening Pop Up stores in 2018 following the acquisition of Whole Foods, Amazon has rolled out a complete physical strategy. However, the company is definitely not in the testing phase regarding its physical-store strategy.

For those interested in knowing, for example, where Amazon Go or Amazon Fresh is available, Amazon stores are mainly located in the US. They can be found in the following Amazon physical store locator. Nevertheless, Amazon plans to expand overseas, with the UK as a testing ground before a full-scale deployment in Europe.

But why the shift? Why is Amazon expanding to formats and delivery modules that are not in natural alignment with its traditional strengths? What’s prompting this retail expansion?

Seven reasons why Amazon is jumping to brick & mortar retail

1. The future of retail is omnichannel

Even though all the talk about the surge in online sales, especially the tremendous spike witnessed during the pandemic, offline commerce isn’t going anywhere.

That’s primarily because the offline shopper behavior of consumers is different from their online behavior. One is driven by experience while the other, by convenience.

This means that there aren’t exclusive groups of shoppers. Instead, most people prefer both kinds of commerce. What they want is a blend – and best – of both online and offline buying experiences.

E-commerce offers an exceptional choice of products, prices, and time-bound discounts that are difficult to find offline. In addition, Offline gives consumers a more immersive shopping experience that’s difficult to replicate online.

The tactile and sensory experience of being in a physical store adds a level of engagement that e-commerce can never compete with.

Amazon knows this and doesn’t want to be seen as just an e-commerce marketplace. They want to be where the customers are.

2. Gathering data on offline shopping behavior

Another reason for the launch and expansion of Amazon physical stores is the enormous data they give the online giant. But, unfortunately, while the company has the shopping data of millions of users, it doesn’t have much on offline shopping behavior.

The online shopping data, while significant, doesn’t tell much about the retail activities of consumers. This isn’t surprising as product search and discovery are different in both spaces.

By focusing only on one, Amazon would be missing out on a completely different set of customer insights.

The Whole Foods deal has to be seen in this context.

This deal gave Amazon detailed data on consumers’ consumption and behavior patterns of a well-established retail brand.

Importantly, it also allowed Amazon to club the benefits of in-store shopping with its Prime membership using refined consumer data.

In that sense, Amazon wasn’t acquiring Whole Foods. It was acquiring its customers.

3. Offline retail offsets shipping costs

Just because they’re a behemoth doesn’t mean rising costs don’t hurt them. Amazon, just like its customers, is always looking to save more. And when your shipping costs are around $61 billion a year, you want to bring it down.

With brick-and-mortar stores, customers would pick up their orders, significantly lowering the shipping costs.

They would also offer easy and inexpensive returns as customers themselves would be bringing back the products.

Also, whenever a customer arrives to either pick up or return a product, an Amazon physical store would be tempting not to check out.

They might find the product they were looking for or a similar one. This, without having to visit another store or open the app and search through several pages.

In other words, an Amazon physical store would double as a retail outlet and a pickup and return center.

4. Rising online acquisition costs

Customer acquisition is expensive whether you’re an independent online brand or the largest marketplace out there. For example, Amazon has to spend significantly on digital marketing to acquire and retain its customers.

And considering the competition and the choices a customer has, it’s a game they have to play repeatedly. As a result, the company has targeted millions of keywords and invested heavily in AdWords and SEO.

But with Amazon physical stores, there won’t be any need to spend to acquire customers repeatedly. Customers are loyal to their convenience or grocery stores and are unlikely to go out of their way to find a new one.

5. Physical store operations are ripe for disruption

If there’s one thing that Amazon’s famous for, it’s disrupting the models and markets it has entered.

And everyone knows that physical stores aren’t exactly known for their efficiency or ease of use. Legacy retailers have some legacy issues.

One could argue that nothing much has changed in the brick and mortar space over several decades.

It’s the same old process of customers locating the products on the shelves, picking them up, heading to a counter, waiting for the cashier to be free, and then checking out.

These are all friction points that Amazon hopes it will be able to solve with its technology.

Automated checkouts, cashier-less technology, and even staff-less stores are just some solutions already part of the Amazon physical store experience.

If those sound innovative, imagine the ability to pay with one’s palm! Now imagine that you can already do it at some Amazon physical stores.

6. A significant share of retail is still offline

Despite the growth of e-commerce, many consumers still prefer their offline shopping experiences.

Contrary to popular perception, online sales have been picking up. Still, they lag behind brick-and-mortar sales in most categories.

According to a PwC Total Retail Survey, 70% of consumers still prefer offline grocery shopping.

While this may not be surprising, what’s notable is that even for clothing and footwear and health and beauty, the majority still would instead buy them from a retail outlet.

So, since Amazon cannot comprehensively change customer behavior, it’s ready to expand its business model.

7. Growing the Amazon ecosystem

Amazon isn’t just the world’s biggest online marketplace.

It’s also an ecosystem of products and services that include everything. From Echo to Alexa to Kindle to payment services to probably self-driving cars in the future.

While the company encourages shoppers to seek its in-house solutions, a retail presence would speed up the process.

Consumers would be more encouraged to buy a Kindle or Echo when they see both in action. Once they roll out the grocery shopping through Alexa, it will elevate their retail game to a whole new level.

Importantly, all these are directed at growing Amazon’s Prime subscriber base. That membership would open up a world of omnichannel benefits to consumers. From shopping to entertainment, all enabled by voice commands.

8 Amazon physical store models you should know about

How has the omnichannel play from the largest e-commerce player worked out so far?

Here are the 9 Amazon physical stores through which the company hopes to revolutionize the retail landscape.

1. Amazon Go

Launched in 2018, Amazon Go relies on advanced machine learning to make shopping seamless for customers. For example, sensors on the shop shelves would inform the system what products a customer has picked up.

The best way to understand the convenience provided by the Amazon Go Concept is to watch this video:

The shopper doesn’t have to check out or approach any counter. Instead, they can head out of the store, and Amazon will automatically charge their accounts. This cashier-less technology is called Just Walk Out and will be explained further in the Amazon Fresh Store section.

This is an excellent example of breakthrough technology. And the company is using it to disrupt an industry notorious for its legacy inefficiencies.

2. Amazon 4-Star

Sometimes it helps to answer questions that no one has asked.

Customers never asked for the highest-rated Amazon products to be available offline.

But that’s precisely what the company did through Amazon 4-Star, which features four-star ratings or above products. These include books, devices, home products, and Echo, to name a few.

Consider it Amazon’s version of a Greatest Hits album.

3. Whole Foods

Whole Foods is perhaps the most high-profile acquisition (before the recent MGM purchase). It was Amazon’s most compelling move to enter the brick and mortar space.

With Whole Foods, Amazon wasn’t just getting close to 500 stores. It also got access to consumers who don’t mind spending extra on organic and sustainable food products.

4. Amazon Fresh Store

If Whole Foods is for more high-end and health-conscious customers, the Amazon Fresh store, previously known as Amazon Go Grocery, is targeted at those consumers who are used to shopping at Walmart or Target. The stores stock a wide variety of products beyond the healthy staples found at Whole Foods.

One of the main innovations implemented by Amazon in its physical stores focuses precisely on Amazon Fresh stores, with the new Just Walk Out shopping technology. Customers opting for the cashier-less technology can use Amazon One to scan their palms, use the QR code with their Amazon app, or insert a credit card linked to the Amazon account. The technology enables Amazon users to shop, pick up the desired items, skip the checkout process, and leave the store freely.

Does this mean that only Amazon users can shop at these new stores? Absolutely not. Anyone can shop at Amazon Fresh, whether using Just Walk Out or the traditional checkout lines paying by cash or a credit card.

5. Amazon Bookstores

No one forgets their first love. And for Jeff Bezos and Amazon, it’s always been books.

Launched in 2015, there are around 25 Amazon Bookstores in the US where customers can enjoy the tactile pleasures of touching and taking in that exquisite aroma that can only come from books.

6. Amazon Lockers

This is one of the finest ways in which Amazon is merging its online and offline brand experiences.

Amazon Lockers can be found in grocery stores, malls, and apartments. After ordering, customers will get a unique code to open the locker and get their product.

Whole Foods has Amazon Lockers which encourage customers to browse their products when they arrive to take their delivery. This is the kind of synergy that Amazon hopes to see across its Amazon physical stores and product portfolio.

7. Amazon Pop-Ups

These are Amazon’s take on casual pop-up stores.

The intent is to make it easy for customers to quickly browse trending products unavailable in stores through interactive displays. Unfortunately, in 2019, Amazon decided to close all its pop-up stores, terminating the experiment.

Nevertheless, later in 2020, Jeff Bezos communicated the strategic decision to reopen the pop-up tests to better understand the physical customer experience and leverage the new data gatherings.

8. Hair Salons

Yes, we, too, were surprised. But at its only location in London, customers can use augmented reality mirrors to know how a style or hair color would look on them.

They will also be given Amazon Fire tablets to entertain themselves. But, of course, they can also buy any cosmetic or beauty product by merely scanning a QR code.

We’re not saying it isn’t a riveting success, but the company doesn’t have plans to open more salons.

Amazon physical stores are the next stage in the evolution of a company with unprecedented domination in one space.

As they get popular, customers would also expect such tech-enabled services from legacy retailers.

It will also emphasize the divide between traditional big-box outlets and a technology-first company like Amazon, precisely what the company wants through its brick-and-mortar stores.

Do you want more insights into E-commerce, Omnichannel Retail, and Digital Transformation? Subscribe to ApocalypseRetail to get insights sent directly to your inbox. Our content is designed for top business schools, retail managers, and eCommerce entrepreneurs who want to survive in the ever-volatile retail industry. Subscribe to our newsletter to join the fight against the Retail Apocalypse!

The post Amazon Physical Stores: A Successful Game Changer in the Retail Sector? appeared first on Apocalypse Retail.

]]>The post Instant gratification: Has Quick Commerce or Q-Commerce changed the way we shop? appeared first on Apocalypse Retail.

]]>We want to give our special thanks to Faraz Kavehei & Johannes Bareis, the two students who co-authored this post.

Quick commerce or q-commerce is completely disrupting e-commerce and Retail.

In this post, we’ll explain this model in a nutshell, introduce key players and analyze the advantages and challenges in the q-commerce industry.

What Is Quick Commerce or Q-Commerce?

Quick commerce, also known as Q-Commerce, is THE big new topic in the retail sector. Covid accelerated the rise of this new delivery model that addresses the consumer’s need for responsiveness and convenience.

Q-commerce changes the entire shopping experience, from the initial spark of interest in a product to the delivery rider knocking on your door.

Wait—you’re thinking—I thought online shopping was e-commerce, not q-commerce.

And you’re not wrong.

Q-commerce is a form of e-commerce, but the turnaround time between order and delivery is much shorter in quick commerce. For example, instead of waiting a couple of days for a product, customers receive their order within one hour, often in as little as 10 minutes.

This is why q-commerce is also called the third generation of e-commerce. On-demand deliveries that are executed almost instantly will be the new benchmark.

Q-Commerce was not born during the pandemic. But the increase in online ordering during the pandemic created the perfect tailwind for q-commerce.

Multiple industries took a severe hit due to the pandemic; q-commerce was one of the few sectors of Retail that flourished when folks had to stay at home. And that change of habit is here to stay.

How Does Quick Commerce Work?

You are expecting a few friends but did not find the time to prepare. You can simply go to the q-delivery app of your choice and order snacks and maybe one or two bottles of wine. About 10 minutes later, a delivery rider will ring the bell of your door.

But how does the magic happen?

Most q-commerce pure players warehouses, so-called “dark stores” or “micro-fulfilment centers.” These dark stores enable workers to quickly pick and deliver the products they have in stock.

Dark stores typically have over 1000 products ready for distribution. These “flash supermarkets” are often placed in strategic locations and act as urban fulfillment centers for a city district.

Until now, it mostly sounds like a regular logistics company that moved a bit closer to the consumer. But Q-commerce players use technology to make their processes more efficient and agile. For example, they use data to understand which locations are better suited to establish dark stores.

They develop specific Order Management Systems to route orders to the closest store to fulfill the order. Next, they match your order with the nearest rider to fulfill your order.

All within 30 minutes or less.

The Quick Commerce business models

There are different q-commerce players all over the world.

All have some specificity, but these are the few common factors:

- Delivery in less than an hour (10min delivery best-in-class)

- Locally focused delivery from dark stores

- A fleet of two-wheeled vehicles to move faster

Most q-commerce retailers are like supermarkets, so-called flash supermarkets.

They have everything from snacks to cosmetics to cleaning products.

Some q-commerce pure players are, in fact, “supermarkets” that hold their inventory. Other q-commerce players work with legacy brick and mortar supermarkets. They are third-party providers that perform the delivery.

What Are the Advantages of Quick Commerce?

1. Speed, Speed, Speed

Speed is the most significant advantage of q-commerce.

The genesis of q-commerce came from the need for ultra-fast delivery in the food industry.

Q-commerce sellers generally don’t have physical locations where customers can walk in and buy things. Still, q-commerce retailers have a unique selling proposition (USP) that sets them apart from competitors.

2. Brand loyalty

Q-commerce today is a commodity.

There are many players, and customers can easily choose from which one to be served.

But it is a winner-takes-all market. Not necessarily globally, but most likely in your district or city.

The one company that can meet customer demands quickly and efficiently will have the most repeat customers.

Customers are more likely to make a repeat purchase from a company that has consistently met their needs.

3. Ultra-fast delivery with 24/7 operations

Dark stores can operate 24/7, leaving no gaps between demand and delivery (given that the local laws permit 24/7 ops)

This makes q-commerce flourish in areas that have limited business hours for physical storefronts.

One of the main benefits of Q-commerce is to order anything you need at any time of the day (or night).

4. Tech-oriented inventory management

With AI and smart technology, q-commerce ensures that products are readily available for people in the area.

Q-commerce software analyses demand trends to help re-shelf stocks based on demand. And even if a product is unavailable for a short period. Then, the app will simply stop promoting that particular product and steer the demand towards other products in stock.

5. It is super easy

Once you’ve tried q-commerce, you understand its ease.

Q-commerce apps generally have straightforward UX/UI. They are built to have super simple sign-in processes and make repeat purchases very easy.

If you forget an item on your shopping trip and don’t want to return it, you can open an app and have someone bring it to you.

You don’t have to take your sweatpants off and put jeans on again.

What Are the Challenges of Quick Commerce?

1. Q-commerce is a commodity

The biggest challenge of quick commerce is staying on top.

All the q-commerce players have a similar model. It all comes down to the best inventory and the best execution.

The number of players existing today makes q-commerce a commodity. As a result, there are almost no switching barriers for customers.

This means that customers have plenty of choices to choose a provider. And it is just as easy to lose a customer as to gain one.

2. Q-commerce customers have Zero tolerance for failure

The primary drawback of ultra-fast delivery is living up to the ultra-fast standard.

It is a market where customers have zero tolerance for failure.

They will only stay loyal if their customer experience is always great.

A player that provides only “good” experiences loses its value and customers.

This is a market that is built on customers that NEED ultra-fast delivery for whatever reason. Unfortunately, these types of customers are the hardest to please.

3. Q-commerce is an extremely risky business model

With such customers, players have to constantly monitor efficiency across their supply chain.

The entire industry is hinged on speed and accuracy for profitability. And as we said before, this is a winner-takes-all market. This means that players need to raise massive amounts of cash to establish operations quickly and win the market.

And the entire business model is based on the availability of staff. Companies cannot scale and maintain their operations without enough riders and pickers available.

Players like Getir, Gorillas, or Flink have provided their staff with employment contracts. Others are still relying on gig workers. However, most countries and cities have started regulating the gig economy, which will impact the business model.

So, in the end, only one or two players will survive per area, and most players will burn through their cash.

4. Convenience often comes at the cost of work conditions

Delivery speed and convenience might come at the cost of agreeable work conditions.

Of course, it’s fantastic to shop for a beer and some snacks at 3 AM on a Tuesday. But there’s someone out there who has to bring you the bag of chips.

And as we said before, parts of the industry are based on the gig economy without full-time contracts or benefits. We’re not saying the gig economy is bad per se. But it has time and time again been proven to offer precarious work conditions.

But riders and pickers also have the freedom to decide where they want to work. Arguably, a job in a classical supermarket is also not more exciting.

In most countries, quick commerce companies would make a strategic mistake to offer lousy working conditions. There is a significant labor shortage in the low-wage sector, and companies have difficulties filling positions.

The food delivery company Wolt offers a sign-on bonus for new riders. An Indeed study suggests that the number of job postings is skyrocketing (e.g., 88% increase in the Loading & Stocking sector).

Companies should not focus on improving margins by reducing labor costs. Instead, they should consider the opportunity costs when they cannot fill positions or have enough riders available.

5. The model might not work everywhere

Q-commerce is mostly available to urban consumers.

The economics of the model is catered to densely populated areas in urban areas. As a rule of thumb, we could say that the sweet spot of the model is in areas with at least four-story buildings.

Some players serve more rural areas but with much longer delivery times. The economics of the model are different outside of the cities.

Additionally, it might not work in every country equally well. Convenience and delivery business models work very well in countries with high inequality (Singapore or Hong Kong). It needs a population segment with high disposable incomes that looks for convenience. And a lower-income population segment that is willing to perform the gig work.

It remains to be seen if the model also works in countries with small Gini-Coefficients, such as Nordic countries.

6. Q-commerce has a significant impact on local and small businesses

Additionally, one of the main casualties of q-commerce is local and small businesses.

It took a global pandemic to get stores to come around to in-store or curbside pickup for online orders.

Stores that are not adopting an omnichannel approach are being crushed.

This is a good thing because most local stores had utterly failed to adapt to changes in customer behavior.

But q-commerce mainly sells items from big supermarkets or big sellers. The type of players who can afford their commissions.

Most local small businesses don’t have the volume or margins to become q-commerce sellers. So a lot of them will inevitably be crushed by q-commerce players.

Is Quick Commerce Profitable?

Short answer: yes, at least in the long term.

There’s a lot of opportunity in quick commerce when executed correctly.

A study from Deloitte revealed that 50% of shoppers spent more money to get what they needed quickly in the heat of the pandemic. Q-commerce players can capture this willingness-to-pay.

In the US, GoPuff is the first-mover. They operate their better warehouses with 40% gross margins and a 10% contribution margin.

Of course, increased competition will put pressure on margins.

100% of GoPuff’s fulfillment centers became profitable after 18 months, and the best ones were even profitable after nine months.

At the same time, classical supermarkets are much more capital-intense and need many years to break even.

Is Quick Commerce Sustainable?

It is hard to prove that q-commerce is more sustainable than traditional shopping. But a few things about it are encouraging.

Deliveries are usually performed with electric scooters or e-bikes. It would be more sustainable if customers would no longer have to get into their cars to drive to the supermarkets or shopping centers.

The way supermarkets work produces significant food waste. Q-commerce has the potential to reduce food waste big time. It has short turnaround times of products. Food can be stored more functional (e.g., dark and cold). It does not have to be displayed in a way that is appealing to customers (e.g., on a shelf with bright light)

Customers do not touch food, and q-commerce companies can also sell the “curved cucumbers” that would be neglected in a supermarket.

Since q-commerce firms are more data-driven, they can better forecast demand. In turn, companies waste less food by ordering the right amount of non-durable products.

Food about to expire could be promoted or discounted on the app. If quick commerce players operate seven days a week, they would not have to deal with fresh food that could get rotten over the weekend.

What is next for Quick Commerce?

Expansion of the product offering

Most players have started with grocery delivery. But their product portfolio will expand to other areas such as OTC (over-the-counter) pharmaceuticals.

After all, we want to stay in bed when we are sick and don’t want to make our way to a pharmacy. Some do this already.

Beyond Groceries, Food, and convenience products

Quick commerce does not have to be limited to food delivery, groceries, OTC drugs, or other convenience articles. It could also solve that last-mile problem in the broader retail industry.

Q-commerce players could also help brands deliver other items like fashion of consumer electronics.

First, start-ups are already addressing this niche. For instance, Arive works with brands like Apple to deliver their products within 30min. The biggest challenge here is inventory. The products can be “flipped” with groceries within 2-3 days. With laptops or designer fashion brands, the warehouses would need to have a lot of expensive inventory. The products need to be readily available in many sizes, colors, or technical configurations.

Reshuffling of the marketing budgets of food companies

Food companies like Kraft Heinz spend a lot of money promoting their brand and products (let’s say a Bacon BBQ-Sauce) to a broad audience.

The demand for their product by customers and their brand image helps them to engage in favorable terms with supermarket chains and retailers.

But their marketing efforts (e.g., in the form of billboards or TV spots) have also targeted consumers that are highly unlikely to buy their Bacon BBQ-Sauce.

Maybe because they are vegetarian or simply do not like BBQs.

Quick commerce players can disrupt marketing in the food industry. Unlike brick-and-mortar supermarkets, they have very detailed information about the preferences and habits of individual customers.

They can monetize that knowledge and address consumers in a much more targeted and effective way.

Own Label products increase margins.

Quick commerce players will be offering their private-label products. They can do this because they have direct access to the customer.

Instead of negotiating with giants like Unilever, Kraft Heinz, and alike, they can offer customers own-label products. This would increase their profit margins.

Who’s Who in Global Quick Commerce

Let’s look at the major quick commerce players currently on the market.

The amount of money being poured into financing rounds for each player gives you a sense of how big the market could be.

GoPuff

The GoPuff business model is considered the q-commerce role model. Based in the U.S., GoPuff brings food, alcohol, over-the-counter drugs, and more to consumers in multiple states.

With micro-fulfillment centers, for a delivery fee of $1.95, shoppers have access to over 3,000 products within 30 minutes.

The company confirmed in July 2021 to have raised $1Bn to expand its global operations. GoPuff is consolidating the market and has acquired competitors such as Dija, Bandit, Liquor Barn, RideOS, Fancy, and BevMo.

Getir

Getir is a Turkish company that started with the speedy delivery of groceries and food from local restaurants.

The company can also provide apparel, pet food, and sex health products within minutes.

The Getir app has raised USD 550M in 2021 to expand to the US and other countries. The acquisitions of Moovand BLOK have accelerated Getir’s expansion.

Weezy

Weezy is a U.K-based grocery delivery service that offers instant delivery within 15 minutes.

It also highlights its stance as an anti-gig economy company, stating that its “riders are more than just riders.”

The company has “only” raised $25M in 2021

Cajoo

Cajoo is a prominent French q-commerce delivery service.

Servicing ten areas in France when we wrote the article, the company specializes in grocery delivery.

In late July 2021, Carrefour, France’s biggest retail company, acquired a minority stake in Cajoo. This investment is for an undisclosed amount.

This investment will allow the Cajoo App to speed up its development. And it will also give Carrefour direct insight to ramp up its delivery operations.

Gorillas

Gorillas is a leading q-commerce start-up and the fastest German company in history to reach the unicorn valuation.

They started their brand to limit food waste by providing fresh food on demand. Their main offer is to deliver in ten minutes or less.

The Gorillas app operates in the UK, Belgium, Denmark, France, Germany, the Netherlands, Spain, Italy, and New York City.

The company has closed a $1B Series C round in October 2021 with the strategic investor Delivery Hero as the lead investor.

Flink

Flink is the second major player from Germany and operates in even more German cities than Gorillas.

The company also expanded to France, Austria, the Netherlands, and Belgium.

Flink is backed by financial investors like Target Global and strategic investors with strong delivery experience such as DoorDash and Prosus.

The start-up has entered into exclusive cooperation with the retail giant REWE Group.

Jokr

Jokr has had extremely rapid growth.

It was founded by the Foodpanda founder Ralf Wenzel and other former Foodpanda and Rocket Internet employees who understand the food delivery market.

They have expanded to dozens of cities in the US, Latin America, and Europe in a few months.

The company has raised $170M in 2021 to expand its global operations.

Glovo

Founded in Barcelona in 2015, Glovo is one of the “old” players in the q-commerce business.

With Delivery Hero as their leading investor, Glovo has become a significant player for on-demand delivery in EMEA markets.

With the rise of q-commerce, Glovo has been investing in its ultrafast delivery capabilities to compete in this market.

They benefit from solid brand awareness and a robust presence in their current markets. So let’s see how they fare in the q-commerce business.

Rappi

Rappi is the Unicorn out of Colombia.

Same as Glovo, the company was a senior player in the delivery business founded in 2015.

The company’s main activities come from on-demand delivery.

They have risen to the top, establishing themselves as the dominant player in Latin America. They have become the most significant player in countries like Colombia, Brazil, or Mexico.

In 2021, they launched a new Rappi Turbo feature, allowing for deliveries in ten minutes or less. This is the start of their q-commerce business.

Again, same as Glovo, they benefit from brand awareness and customer loyalty in their current markets. It will be exciting to see how they compete in the quick-commerce business.

What will Amazon do in quick commerce?

The retail giant Amazon is currently standing on the sideline regarding quick commerce. For example, its fastest service Amazon Fresh needs about 2-3 hours of delivery time in major cities.

Going forward, there are two possibilities for how Amazon will (re-)act.

- They will wait and acquire the leading quick commerce player

- They will choose a different strategy (just-in-time instead of instant on-demand delivery)

Amazon could also decide not to become part of the quick commerce race.

They are still way ahead regarding access to the customer and their household (think Smart fridges and Alexa). Amazon could bet on the convenience of automatic restocking. Your milk or guacamole could be delivered and restocked just in time before your current container is fully consumed.

Conclusion:

There may be a lot of challenges ahead for Q-commerce.

The market will consolidate, but several players might dominate in a specific city or area.

So we do believe q-commerce is here to stay and will only grow in popularity. It educates consumers and changes consumer demands in the long run.

But we are thrilled to see who comes out on top in the long run.

If you know other players to include in this list, drop us an email, and we’ll add them.

Do you want more insights into E-commerce, Omnichannel Retail, and Digital Transformation? Subscribe to ApocalypseRetail to get insights sent directly to your inbox. Our content is designed for top business schools, retail managers, and eCommerce entrepreneurs who want to survive in the ever-volatile retail industry. Subscribe to our newsletter to join the fight against the Retail Apocalypse!

The post Instant gratification: Has Quick Commerce or Q-Commerce changed the way we shop? appeared first on Apocalypse Retail.

]]>The post Is Black Friday Dead Yet? Here are Black Friday Alternatives to Empower Ethical Shoppers appeared first on Apocalypse Retail.

]]>Black Friday has become a day that, for many people, symbolizes a celebration of consumerism. It is the unofficial start of the Christmas shopping season that has become a landmark event for retailers.

For some retailers, it comes with increasing profits. For others, it can become a logistical nightmare.

Their aggressive discounts and promotion strategies send consumers into a frenzy.

Everyone has seen the pictures of people camping outside stores before opening, and even cases of people trampled by crazed shoppers.

But looking beyond consumer craziness, Black Friday and other mega sales events have been a target of critics for more sustainability in Retail.

These critics argue that mega sales events encourage excessive and often unnecessary consumption, which has severe environmental and social impacts.

Let’s look at what mega sales events are, how they started, and how big they have become. We’ll also look at these events’ environmental and social impact and what Black Friday alternatives exist for more ethical consumers.

Why is it called Black Friday?

The Philadelphia and New York police in the fifties named the day after Thanksgiving Black Friday.

As a US holiday that occurs on a Thursday, many people would take that Friday off work to have a long Thanksgiving weekend with their families.

During Thanksgiving, most people exchange gifts, so retailers would stock up in certain products the month before the holiday.

In the beginning, retailers used Black Friday as an opportunity to clear out excess inventory by discounting it. By clearing out excess inventory, retailers could make room for new products within stores for the Christmas season.

So it was during the fifties, shoppers began to flock into the city to start their Christmas shopping.

As consumers gathered in the city to find the most discounted items, the event started requiring more police enforcement. The police had to work longer hours and handle the chaos; they dubbed the Friday after Thanksgiving Black Friday.

But the dynamics of the event have evolved over the years. Black Friday stopped being a stock-clearance event for retailers and started to include high-demand items to attract more shoppers.

On top of this, Retailers started to entice shoppers with more aggressive discounts and significantly increased their advertising of the event.

It was really in the 1980s that Black Friday became a frenzy in the US.

People would queue outside department stores for hours or overnight to be the first ones into the shops. Security and law enforcement had their work cut out trying to contain the crowds fighting each other to get their hands on a discounted TV.

Seeing the potential for increased sales, retailers kept investing in Black Friday, and the trend started spreading worldwide.

And other mega sales events started popping up.

What are Black Friday Equivalents as mega sales events?

As Black Friday became a staple of American Retail, other mega-sales events started popping up worldwide. In some cases, these events are pushed by a single company or were based in a single country.

With the rise of e-commerce and a more interconnected Retail, most of these events have become global.

With Retailers everywhere aiming to take a cut of mega-sales events, some events have become very popular. But there are really three mega-sales events that are comparable to Black Friday in terms of size and reach:

- Cyber Monday or Black Friday Weekend

- Singles’ Day or 11-11

- Prime Day

What is Cyber Monday or Black Friday Weekend?

Cyber Monday happens on the Monday just after Thanksgiving and just after Black Friday.

With the frenzy of Black Friday and the resources it takes in terms of law enforcement and consumer protection, cities have begun regulating Black Friday.

In some cities, not all stores were allowed all day, and retailers had to follow specific rules for what could be advertised as a Black Friday deal. For example, to be considered as a Black Friday deal, some items needed to have a minimum amount of stock or an unchanged price for some time before the discount.

The idea was to protect consumers from false advertising.

But with the rise of online shopping and many stores wanting to avoid the Black Friday crowds’ craziness.

In 2005, the National Retail Federation in the US officially dubbed Cyber Monday after a trend that retailers began to recognize a few years before.

Online Retail is not bound by the same constraints of physical Retail to have a limited stock per store or fixed opening hours.

So Cyber Monday allowed retailers to continue Black Friday deals one more day, with a less stringent regulation as fewer public resources are required.

Today, most retailers mix deals between Black Friday and Cyber Monday. The event has really become a Black Weekend, with sales running for four days.

For some retailers, revenues generated during Black Weekend can concentrate up to 20% of their entire year revenues. So this weekend can literally make or break a year’s performance for these companies.

Some e-commerce pure players have even started to push deals during the week with what they call Cyber Week, a term that appeared in 2013.

What is Singles Day or 11-11?

As profitable ideas are quick to spread, other countries started to catch on to the benefits of mega sales events.

The original idea came from an unofficial holiday in China to celebrate people who are not in a relationship.

The date was chosen on November 11th as 11-11 as the number 1 symbolizes an individual or a single person. The number 1 also resembles a stick used in Chinese slang to refer to an unmarried person.

Paradoxically, the date has become a massive event to celebrate weddings and give gifts which have greatly benefited online players such as Alibaba or JD.com.

This massive online shopping event recently surpassed Black Friday and Cyber Monday sales as the world’s largest mega-sale event.

With Chinese companies becoming global, the Singles’ Day event has spread to the rest of Asia and elsewhere.

Companies like Lazada in South East Asia, MediaMarkt in Europe, or Aliexpress (a global arm of Alibaba) have made Singles’ Day campaigns across different countries.

These companies have pushed to make this event an actual global mega-sale event.

What is Prime Day?

Amazon has been one of the biggest retailers benefiting from the Black Friday and Cyber Monday sales.

But same as any other retailer in the consumer goods industry, Amazon is highly dependent on the holiday season during Q4.

In 2015, Amazon introduced the concept of Prime Day with a single promise: “Offer Black Friday deals in July” exclusively for members of their loyalty program.

Of course, Prime Day is an opportunity to attract shoppers during the “slow-season” of Retail during the summer.

It is also a great way to offer an additional incentive for amazon shoppers to subscribe to their loyalty program, Amazon Prime.

But from a strategic standpoint, it has two additional benefits for a company like Amazon. On one side, it allows the company to absorb fixed costs during the off-season as most of the operational structure is under-utilized. On the other side, it is a great way to test new features and processes before the high season.

Amazon has continued pushing Prime Day sales every year since 2015 and has deployed it in every single country they operate.

Mega-sales events have become critical dates in global Retail.

But as consumers become increasingly aware of the impact of mass consumption, many people ask if these events are compatible with more sustainable Retail.

Are mega-sales events compatible with sustainable Retail?

There are critics of Black Friday and other events in some European countries for being “too American.” These critics are easily dismissed, and these events have found many supporters across Europe

But these events are also being criticized as being the flagships of overconsumption.

Black Friday and mega-sales events are the flagships of overconsumption.

As consumers become more socially responsible, they realize that there is an impact of having mega-sales events.

It is impossible to separate the environmental cost of mega-sales events from the impact of general overconsumption.

Mega-sales events are built around heavy marketing campaigns and the scarcity factor of limited-time deals.

You could argue that the entire event is built around pushing consumers to buy items using time-sensitive deals. But, in turn, these deals inevitably promote waste as people buy things they don’t need and unnecessarily use more resources.

Supporters of mega sales events say that they give people with limited means access to products they wouldn’t otherwise be able to buy.

They will also argue that Retail companies need these events to clear out stock or reduce dependency on the high season.

Let’s not forget that this was the reason Black Friday started.

But the reality is that Black Friday has turned into a much bigger event with higher marketing spend and shopper frenzy, far from its original purpose.

Today, Black Friday has become a race to increase revenues, extending deals as much as possible to promote consumption.

There is nothing sustainable about overconsumption.

Black Friday and mega-sales events have a tremendous impact on retail employees.

Black Friday and other mega-sale events are a logistical nightmare.

For online and offline retailers, preparing for a mega-sale event can take an entire year.

There is stress involved in preparing for the event. Stress comes from making sure you have the right amount of stock at the right place, pushing aggressive marketing campaigns, and working much longer hours than usual.

But there is also the stress of dealing with frustrated customers, which have even put lives at risk. There have been reports of brawls, fights, and even deaths related to Black Friday in the US, Brazil, or Mexico.

With the rise of social media, more and more videos surfaced of brawls in 2017 and mall shootings in 2019.

These events alone are enough to make people question if these mega-sales events are sustainable.

Questions come not only from an environmental point of view but also from a corporate social responsibility standpoint.

Retailers should ensure the safety of their customers, as well as the security of their employees.

Ensuring customers’ safety has become a challenge during these events, especially during the effects of the Covid19 pandemic, with social distancing guidelines and other public safety measures.

So on top of questions regarding overconsumption, Black Friday and other mega-sales raise questions as public safety hazards. Which in turn raises questions about the sustainability of these events over the long run.

With the pandemic, some of them really thought it was the perfect storm to kill Black Friday once and for all.

The impact of Covid19 on Black Friday: longer deals and more online shopping

The Covid19 pandemic did have an impact on overall retail sales, forcing the closure of stores.

Public safety measures inevitably hurt the overall number of shoppers during Thanksgiving weekend.

But Black Friday remains a huge Retail event worldwide.

How big was Black Friday 2020? It slowed a bit but remains huge!

Thanksgiving weekend includes the five days between Thanksgiving and Cyber Monday, including Black Friday. As a result, these five days have become a single mega-sale event worldwide.

According to the National Retail Federation, Thanksgiving weekend attracted 186.4 M shoppers in the US in 2020. This number is down from 189.6 M in 2019 (-1.7% ’20 vs ‘19), but up from 165.8 M in 2018 (+12.7% ’20 vs ’18).

In terms of revenues, Thanksgiving weekend totaled $58.1B in 2020. This number is down from $68.6B in 2019 (-15% ’20 vs ‘19), but up from $51.9B in 2018 (+11.9% ’20 vs ’18).

So, it becomes clear that in 2020 the growth of Black Friday was slowed by the pandemic. But the reality is that most consumption instead transferred online, with a massive increase in e-commerce sales during the pandemic.

The Covid19 has far from killed Black Friday; instead, it has transformed it.

Black Friday and Cyber Monday are becoming global events for online shopping.

The covid19 pandemic had a negative impact by slightly reducing the number of shoppers in the US in 2020. But it had another significant effect on how these shoppers made their holiday purchases.

According to the NRF, online shoppers during Thanksgiving weekend in the US increased by 44% in 2020 compared to 2019. If you consider only Black Friday, the number of online shoppers during this particular event surpassed 100 M for the first time ever.

If we analyze Black Friday and Cyber Monday numbers globally, online players are evidently thriving during mega sales events.

During Black Friday and Cyber Monday, Amazon totaled $4.8B in Gross Merchandise Value globally, up 60% from 2019. Another player that thrived was Shopify which racked up to $5.1B in Gross Merchandise Value globally, up 75% from 2019.

The interesting part about Shopify is that the company generated triple-digit growth in European countries where Black Friday has been most criticized. Shopify sales grew in Italy +211%, Germany +189%, and UK +122%

Interest for Black Friday in 2020 varied globally

Perhaps one of the best ways to measure where Black Friday has the most strength is by looking at online searches.

According to Semrush, Black Friday’s global interest varied considerably between countries.

Online searches for Black Friday-related keywords grew by +34% in countries like the US and Australia, with a peak growth in searches in Brazil, where it reached +48% in 2020.

On the other hand, interest in Black Friday seems to be stalling in European countries. The countries where interest for Black Friday dropped the most were Germany, France, and Spain, where searches dropped by -16%, -4%, and -2%, respectively.

Covid19 transformed how traditional retailers addressed the pandemic.

Giant retailers with physical stores used the opportunity in 2020 to change how they operated during Black Friday.

To promote public safety and limit the number of people in stores, retailers like Walmart, Target, or Home Depot made significant changes to their black Friday deals.

Instead of concentrating on a single weekend, they pushed for month-long deals or divided into smaller sales events during the season.

These companies, which have many shoppers visiting their brick-and-mortar stores, worked to offer a safer shopping experience.

The main changes from brick-and-mortar retailers during Black Friday 2020 included:

- longer opening hours,

- limiting the number of shoppers per store,

- promoting curbside pick-up

- making deals available for several days to avoid in-store congestion.

Walmart, for example, divided Black Friday 2020 into three separate events and opened their stores at 5 am during these events. As a result, the campaign was called “deals for days.”

So, the reality is that big Retailers are moving away from Black Friday, but not because of corporate social responsibility. Instead, they are moving away from Black Friday to reduce the risk of a single concentrated event which has become a logistical nightmare.

How big are Singles day and Prime Day?

Short answer: they are huge, and they keep growing.

In 2020, all the major players involved in these events broke records in terms of gross merchandise value and the number of products sold.

During Single’s Day 2020, Alibaba and JD.com made more than $115B in revenues, with Alibaba making $74B (+26% vs. 2019) and JD.com making $41B (+33% vs. 2019). At the height of the event, a record number of 583k orders per second were recorded.

Yes, you read these numbers correctly. In 2020, these two companies alone generated more volume than the entire US Retail thanksgiving weekend 2020 combined!

During Prime Day 2021, which was held at the end of June, Amazon totaled $11.9B worldwide, up 7.6% from 2020. To give a sense of the event’s magnitude, the company founded by Jeff Bezos shipped more than 250M items during Prime Day 2021.

In other words, the global volume for Prime Day 2021 was almost 2.5x as big for Amazon as thanksgiving weekend 2020. Very few companies can create a global mega-sale event of their own and make it even bigger than Black Friday.

Despite the environmental and health concerns, 2020 Mega-sales events broke records worldwide.

One could even argue that despite a slight decrease in foot traffic in 2020 due to the pandemic, Black Friday and other mega-sales events are bigger than ever.

And forecasts for 2021 predict an even higher volume as consumers are flocking back to the stores.

But if we consider searches related to Black Friday, keywords related to sustainable black Friday alternatives are increasing sharply.

According to Semrush, online searches for “shop sustainably” and related terms grew by an average of over 650% between 2020 and 2019.

It seems that consumers are more interested than ever in looking for Black Friday Alternatives. So, what can consumers do?

Brands are offering Black Friday alternatives to answer consumer interest in sustainable shopping.

It’s clear that when consumers start to care about something, brands follow.

A 2019 survey from Hotwire found that 47% of internet users worldwide claimed to have switched to a different product or service because the company that made them violated their values.

In this sense, brands worldwide embrace the rising consumer interest in Sustainable Shopping, which illustrates a significant shift in consumer behavior.

To attract a more environmentally conscious consumer, certain brands are launching Black Friday alternatives.

Some of these alternatives can be considered as pure green-washing campaigns.

Companies are readjusting their strategies instead of competing during Black Friday, which is a logistical nightmare and has high traffic-acquisition costs.

Some companies argue it’s driven by a mission to stop hyper-consumerism as flash deals often lead to rushed purchase decisions.

But these companies are not stopping sales. They are making longer, less aggressive deals, benefiting their bottom line while getting great PR

True hardcore sustainability stems from only buying what we need and then making good use of it for as long as possible.

This makes it challenging to balance the temptation for increasing sales with taking environmental actions.

We have selected a few alternatives that seem to stick true to the core values of retail sustainability: environmental and social responsibility.

5 Black Friday alternatives to empower ethical shoppers

First and foremost, we understand the best alternative to black Friday is simply to not purchase anything during that period.

But since it is just before the holiday season, chances are you are looking for gifts to give, or maybe for items you need.

Here are what we think are the Black Friday Alternatives for sustainable shopping available today. If you have any other, don’t hesitate to tell us!

1. Buy Nothing Day

As we just said previously, an authentic hardcore approach to sustainable shopping would be to boycott Black Friday entirely. And not just Black Friday, but all mega-sales events during the year which promote hyper-consumerism.

In this sense, the most obvious alternative to Black Friday is simply to buy nothing on that day.

This movement was born in 1992 in Vancouver, Canada, which has since spread to multiple countries in Europe and America.

On their website, they argue that “The simplest way to celebrate is, of course, to avoid making any purchases on the day. That means dodging the Black Friday sales, no quick trips to the grocery store, no online purchases, etc. “

The passive approach is simply to buy nothing on Black Friday. Still, the Collective has since taken a more militant approach to organizing protests to draw attention to overconsumption.

They have organized credit card cut-ups, where participants stand with scissors on shopping malls, cutting credit cards as a sign of protest. Another creative form of protest is what they describe as the zombie walk, where participants wander around in stores with a blank stare.

2. Recommerce: making retail circular

Recommerce or Reverse Commerce is a significant trend impacting Retail today. It can basically be summed up as purchasing (or selling) second-hand items.

Over the past years, certain online players have grown tremendously by allowing customers to sell or purchase their second-hand items.

Within the fashion industry, players like Vinted or Vestiaire Collective in Europe have demonstrated the true potential of second-hand fashion.

In other industries, some players have taken reverse commerce to the next level. Companies like Craigslist, LeBonCoin in France, or Wallapop in Spain allow millions of transactions of second-hand items from almost any kind.

Finally, other companies have taken full advantage of the refurbishing business model to offer a second life to pre-used items.

A company like BackMarket offers refurbished electronics items to tackle waste in the electronics industry.

In the car industry, companies like Carvana, Cazoo, or Kavak are refurbishing used cars to extend their life and offer a more sustainable alternative to buying new cars.

The concept of ReCommerce is not really something new, but with the help of technology, it can reach new heights.

Sin 1989, the concept of ReCommerce was already at the heart of protests and support songs.

In the words of Pete Singer in his song to support environmental policies in the city of Berkley in 1989: “If it can’t be reduced, reused, repaired, rebuilt, refurbished, refinished, resold, recycled, or composted. Then it should be restricted, redesigned, or removed from production.”

3. Brands donating proceeds during Black Friday

Eco-friendly veterans, Patagonia, have long fought against the linear economy. Instead, they design products using recycled plastic and repair and resell used goods to stop them from landfills.

Patagonia was a pioneer in pushing back against the consumerism of Black Friday. Their viral campaign told consumers “Don’t buy this jacket” back in 2011, reminding people only to buy what they needed.

Five years later, Patagonia notoriously committed to donating 100% of their Black Friday sales to grassroots environmental organizations worldwide, which ended up being $10 million, over five times their original estimation.

Patagonia has been involved in these kinds of actions for a long time. The founder of Patagonia, Yvon Chouinard, and the founder of Blue Ribbon Flies, Craig Mathews, started the 1% for the Planet initiative back in 2002.

The initiative aims to prevent greenwashing and certify donations that effectively go to protecting the environment. The 1% for the Planet certification is given to businesses and individuals that donate 1% of annual turnover or salary to environmental causes

4. Brands closing stores and telling consumers to #OptOutside

Another outdoor goods manufacturer, REI, has also been battling Black Friday for many years now.

They close their stores so that their employees can spend the day after Thanksgiving with their families and encourage shoppers to join in the #optoutside campaign.

The idea is to spend this mega sales day enjoying the outdoors instead of giving in to the temptation of compulsive shopping.

Even if the campaign was initially created for Black Friday, the #OptOutside hashtag has been used frequently on Instagram with over 18M posts.

Another brand that took a decisive stance against Black Friday is the US skincare brand Deciem.

During Black Friday 2019, the company closed all its stores and blacked out its website with a message saying: “We no longer feel comfortable being involved in a single day so heavily focused around hyper-consumerism.”

The brand became known for its stance promoting slow shopping, making less aggressive deals during more extended periods to remove the element of time pressure. In turn, they argue their customers have time to shop more mindfully.

5. Make Friday Green Again Collective

As a response to the environmental impact of Black Friday, there are also European initiatives like the Make Friday Green Again collective.

The Collective is a group of 400+ retailers and e-commerce players in Europe committed to making Black Friday environmentally friendly. The movement is the brainchild of Nicolas Rohr, one of the co-founders of eco-friendly clothing company Faguo.

All members decided to opt-out of Black Friday discounts. These encourage consumers to buy on impulse instead of what they need.

Instead, their campaign aims to make consumers think about their clothes’ environmental impact during their whole life cycle.

Their message was to use Black Friday not to shop but rather as a day to review our closet to see what we can still use, recycle, repair, or resell.

This way, we make sure we extend the life of our existing clothes before giving in to the temptation of significant discounts.

Many of the brands that collaborate with them are moving from fast to “slow fashion” or “slow shopping. They educate consumers to buy fewer items but of better quality and more responsibly made.

There is an undeniable rising interest in sustainable shopping. With more and more consumers asking questions about what they’re buying, who they’re buying it from, and their values, retailers can benefit from taking note.

Nevertheless, it is also clear that Black Friday and other mega-sales events are still a massive deal for the global retail industry.

Some brands are making small, superficial efforts to make their overall campaigns more sustainable to answer consumer demands. Other smaller, more militant brands are taking measures to the next level to educate consumers and boycott Black Friday.

Only time will tell how consumer interest varies over time and if the rising critics to mega-sales events make Black Friday finally stumble.

Do you want more insights into E-commerce, Omnichannel Retail, and Digital Transformation? Subscribe to ApocalypseRetail to get insights sent directly to your inbox. Our content is designed for top business schools, retail managers, and eCommerce entrepreneurs who want to survive in the ever-volatile retail industry. Subscribe to our newsletter to join the fight against the Retail Apocalypse!

The post Is Black Friday Dead Yet? Here are Black Friday Alternatives to Empower Ethical Shoppers appeared first on Apocalypse Retail.

]]>The post How to compete with a big Retailer? Short answer: provide a better experience! appeared first on Apocalypse Retail.

]]>An improved purchasing experience resets the expectation level on all purchasing experiences. This is the hard truth of 21st century retail, and especially after the impact of the Covid19 pandemic on retail.

It is true whether you buy from an e-commerce pure-player, from your local store, or a big Retailer. So whether you are a small retail store or a growing e-commerce player, all companies are playing by the same rules.

But not all companies have the same budgets, so it can appear daunting to enter the Retail market when there are many established players.

Traditional retailers only provide an average or good customer experience.

The reality is that today, most Retail customer experiences are only rated “OK.” Only a few are rated as “Good,” and none are “Excellent.”

This is one of the reasons to explain the Retail Apocalypse with traditional brick-and-mortar retailers closing stores and filing for bankruptcy.

When you, as a customer, experience something new and refreshing, what do you do? You will automatically compare all your following experiences to that particular refreshing experience.

This customer behavior is nothing new in retail. Customers have always been attracted to over-the-top experiences. This is what made brands like Disney or Starbucks so famous during the 80s and 90s.

Still, for digital customers, expectations are higher and higher every day. And these expectations are higher on every single channel that customers use.

This is where many Retailers struggle to provide great experiences for their customers.

We’re not saying good or OK experiences in every channel. We are referring to GREAT experiences in every channel.

You know which experiences we are talking about, no?

We are talking about those experiences that generate a “wow-effect” on customers, and they want to share with their friends.

How to compete with a big retailer: Anyone can enter the Retail Market, but not everyone can provide a great experience.

In today’s Retail, almost anyone can launch an online Retail (e-commerce) business. There are no coding skills required anymore.

You don’t even really need loads of cash to start. You just need to have time and curiosity.

But it might seem daunting to enter a market to compete with huge companies with big budgets. So how to compete with a big Retailer, whether online or offline?

The answer is simple: provide a better experience than them.

This is something that students and startup founders often think it’s very difficult. They get understandably worried by the cash aspect of competition.

The reality is the bigger the company, the slower they are. This lack of speed comes from inefficient structures and organizations. These inefficiencies make it incredibly difficult for a big company to provide great experiences.

Or at least not on a consistent level across all their channels.

For big retailers with stores, most of the great experiences for customers come from the physical touch-point. In particular, from that store employee who went the extra mile.

This is often the result of a specific human interaction rather than a consistent process across a store network.

Retailers invest massively in training their store employees to provide outstanding customer experiences. This investment can provide excellent results if done correctly. Still, it’s costly to do at scale, and it is a long-term game.

This is the reason that makes “wow experiences” scarce among big Retailers. The capacity to provide extraordinary experiences is where a smaller player has an edge.

Digital native companies are often born with an exceptionally accurate view of their customers. From the start, these companies implement tools to track and analyze customer behavior.

With these tools, small companies create more meaningful connections with customers.

Which leads to a higher rate of “wow experiences.”

Providing great experiences implies a deep understanding of your customer base.

We’ve seen success stories of companies that go from zero to millions in a few years. Companies that start from scratch and have hyper-growth through different growth hacking techniques.

Growth hacking became a buzzword for entrepreneurs looking to grow quickly. But at the heart of growth hacking, there is an unavoidable step if you want to succeed.

You need to have a deep understanding of your customer or a 360 view of the customer.

It’s not just their demographics like age and location. You have to understand their journey, interests, pain points, intentions, context, etc.

Small, focused companies tend to provide consistent customer engagement across channels. They actively aim to provide that “wow effect” during different journey steps.

DNVBs don’t focus on having customers; they focus on having fans. So they make an effort to provide a great experience.

This effort implies a deep understanding of their customer base across all channels. This is where most big companies fail to bridge the gap across channels.

Most of the time, retail managers want to provide consistent engagement. Still, they rarely do it because of outdated systems or complicated internal processes.

This is why big companies offer a better experience in a single channel. In their organizations, big retailers often separate the online from the offline revenue.

This leads to a different experience by channel, almost always benefiting the offline experience. This happens because resources are allocated to the channel that brings the most revenue.

By doing this, Retailers focus on having generous loyalty programs or training store employees, often forgetting to make all these investments in every channel. The problem is that today the lines get blurred between online and offline Retail.

The customer behavior today is omnichannel. The customer jumps seamlessly from one channel to the other depending on their context and needs.

And the purchasing experience is constantly improved by smaller, more agile companies.

This means big retailers have to do much more work than they used to provide a great experience. But big retailers are not used to this much effort to make a sale.

For almost three decades, asymmetric information benefited Retailers against customers. But today, customers have a smartphone in their pocket. So they turned the tables on who controls the information.

This means that today, customers have complete control of when, where, how, and whom they want to buy from.

So whether you are a small or big player in Retail, you have to put in the work to offer a great experience. This is the real answer on how to compete with a big retailer.

This means generating long-standing impressions on your customers and providing a consistent experience across channels.

Do you want more insights into E-commerce, Omnichannel Retail, and Digital Transformation? Subscribe to ApocalypseRetail to get insights sent directly to your inbox. Our content is designed for top business schools, retail managers, and eCommerce entrepreneurs who want to survive in the ever-volatile retail industry. Subscribe to our newsletter to join the fight against the Retail Apocalypse!

The post How to compete with a big Retailer? Short answer: provide a better experience! appeared first on Apocalypse Retail.

]]>The post What is the Retail Apocalypse? The End of Traditional Brick-and-Mortar Retail appeared first on Apocalypse Retail.

]]>In particular, the shifts in consumer behavior over the last two decades. In this period, there has been a massive shift in access-to-market for Brands.

Traditional brick-and-mortar Retailers have (mostly) failed to adapt to this shift. As a result, traditional retailers have legacy IT systems, outdated acquisition tactics, and rusty supply chains.

Very few companies made investments to update their infrastructures.

The majority just kept doing the same thing that had worked during the Golden age of traditional Retail.

Then the Covid19 pandemic struck in 2020 and a lot of traditional retailers were spectacularly underprepared to meet the demands of the new customer behavior.

What is the Retail Apocalypse? Understanding the golden age of brick-and-mortar Retail

From the 80s to the early 2000s, wholesale brick-and-mortar Retailers dominated the market. They became what we know as Traditional Retailers or Legacy Retailers.

During three decades, these companies were THE channel for customers to access products and brands.

There was a clear separation of roles.

On one side, brands that designed and made products. On the other side, brick-and-mortar Retailers, which provided access-to-market to reach customers.

Traditional Retailers dominated every single Retail category. If you had a brand and wanted to have mass access-to-market, you needed a brick-and-mortar retailer. Most retailers specialized by category or by target audience.

Companies like Leroy Merlin, Home Depot, or Bauhaus specialized in the Home Improvement category. Companies like Galeries Lafayette or El Corte Inglés targeted more premium urban customers instead of a single product category.

Traditional retailers based their leverage on dense networks of physical stores. Networks were built across regional, national, and sometimes international levels.

Wholesale retailers became the gatekeepers for any brand that wished to sell a product for mass consumption. Retailers which thrived were disruptive and became dominant in their category or region.

They were disruptive in their approach to the customer experience. Generous loyalty programs and return policies helped them build trust with consumers. In turn, they built a strong and recurring customer base.

Their store network allowed them to have a local-based marketing approach. Traditional retailers built their strength on a close connection between store employees and their customers.

This connection gave them significant control over information on both brands and customers.

Information control turned to higher margins and higher profits.

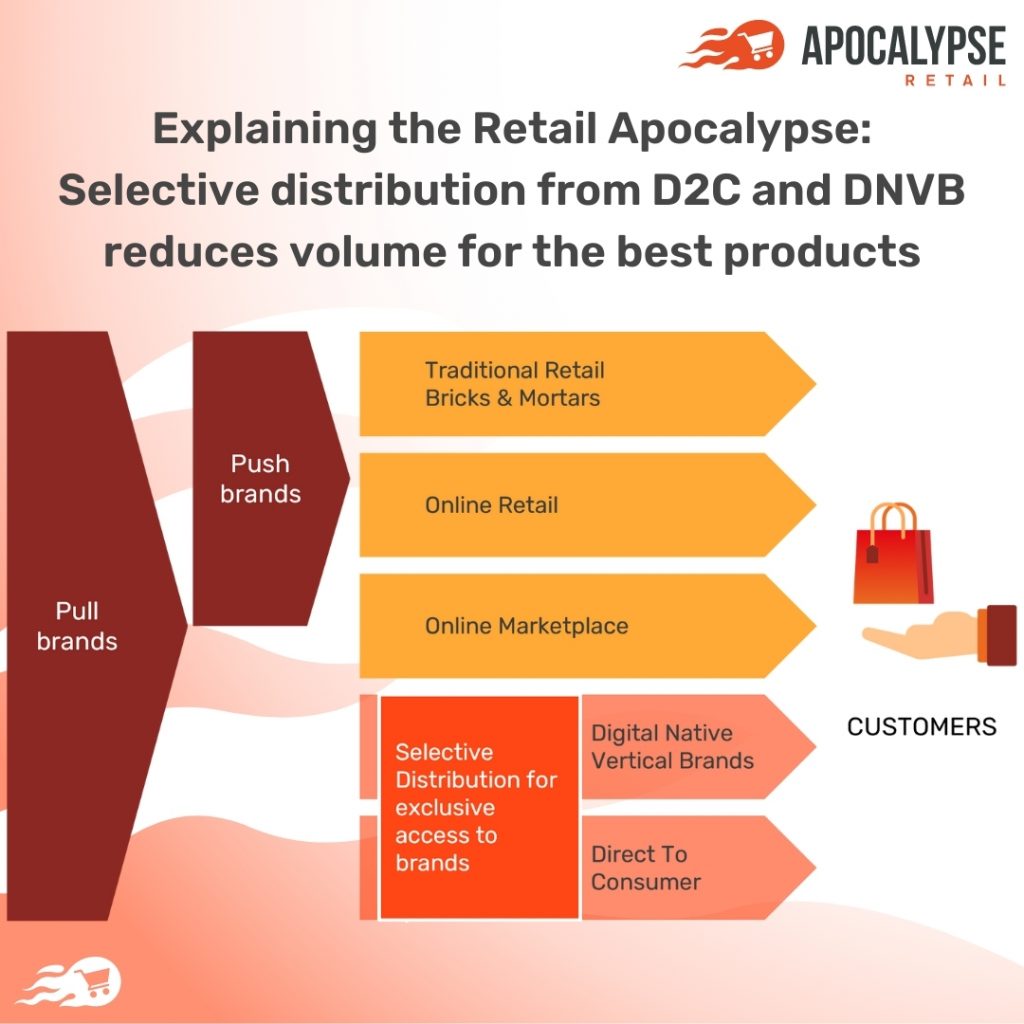

But in the early 2000s, two significant changes put an end to Traditional Retailers’ dominance. The first one is the significant expansion of D2C commerce, and the second one is the rise of online shopping.

1. The rise of Direct-To-Consumer (D2C) Retail

Brands that had enough pull to attract customers began establishing their own stores. These pull brands began cutting out the “middleman” and started reaching directly to customers.

Apple stores are the perfect example.

By 1999, Steve Jobs had returned for two years as Apple CEO. Unfortunately, he was less than happy with the customer experience provided by Retailers like Circuit City or Office Max.

He believed that the brand needed to have closer control over the presentation of its products. At this point, he built a team to venture into physical Retail.

By 2001, Apple opened its first two stores in the US, introducing clean, experience-based stores.

In all categories, brands began opening physical stores to reach customers directly. Categories like sports, fashion, luxury, or cosmetics have seen the most significant changes.

This trend has been accentuated in recent years.

Huge companies like Nike, Adidas, Nestlé, Unilever, or L’Oréal are taking the DTC route. These brands were dependent on wholesale retailers, but not anymore.

According to different reports in Modern Retail, Digiday, Retail Dive, these brands will generate over half of their revenues from DTC by 2025.

This is one of the root causes to understand the end of traditional Retail and what is the Retail Apocalypse. If you want to read more about established brands embracing DTC, read this post.

2. Technology multiplied channels for access-to-market

Way before the Covid19 pandemic, the internet and, in particular, mobile technology completely disrupted access-to-market for brands.

A new breed of Retailers used technology to implement new fulfillment methods and customer engagement strategies.

E-commerce appeared as a new distribution channel to increase competition for physical retailers. Before e-commerce, it was pretty straightforward for Retailers to identify their competitors.

At a local level, it’s easy to notice if a newcomer enters the market. It’s also easier to watch aggressive promotions or activities from competitors.

Online Retailing E-commerce changed these dynamics with new players.

New players such as online pure players, online marketplaces, or DNVBs multiplied competition for traditional retailers.

Let’s deep-dive into these different types of players to understand their impact on the Retail Apocalypse better.

What is an Online Marketplace?

Online Marketplaces appeared at the end of the 90s but got traction at the beginning of the 2000s. These players used technology to connect sellers to customers.

What is an online marketplace? An online marketplace is a platform that connects sellers of a specific product with customers for that product.

At its core, an online marketplace creates value by offering three services:

- A robust technological platform able to onboard thousands of sellers

- High traffic acquisition capabilities on the platform

- Healthy conversion rates for the products within the catalog

A marketplace operator is not the owner of the product. Also, the operator doesn’t necessarily have the physical stock of the product.

In exchange for its services, an online marketplace takes a commission per transaction. Sometimes, the marketplace also charges a fixed fee to use the platform.

An online marketplace can be compared to a shopping mall that runs only online. Still, there are significant differences in the customer journey and monetization business models.

Online marketplaces appeared in the middle of the 1990s. Amazon and eBay were created in the US in 1994 and 1995, respectively. By 1999, the model was exported internationally with the creation of Mercado Libre in Argentina and Alibaba in China.

The Amazon case is a bit different since it started as a Book Retailer Online.

In its early days, Amazon operated as an online retailer, being the owner of the books it sold. Later, Amazon shifted to a marketplace model connecting booksellers to customers.

During the 2000s, all these Marketplaces consolidated their positions as e-commerce leaders. As a result, most of the growth in their respective retail markets was captured by these players.

This growth was almost always at the expense of the traditional retailers competing in the same categories.

In the late 2000s, a new breed of online Retailer appeared: Digital Native Vertical Brands (DNVB).

What is a Digital Native Vertical Brands (DNVB)?